The financial landscape has undergone a remarkable transformation in the past decade, predominantly driven by rapid technological advancements. These innovations have not only revolutionized the way financial services operate but have also paved the way for a new breed of players in the market—fintech lenders. Unlike traditional financial institutions like banks, thrifts, credit unions, and finance companies, which have long dominated the personal loan sector, FinTech lenders leverage cutting-edge loan origination technologies to streamline processes, enhance user experiences, and offer more personalized financial products.

This shift towards technology-driven financial solutions has opened the market to an increasing number of players, each bringing fresh perspectives and innovative models to the sector. The entry of these new players has been facilitated by the democratization of financial services, where technology lowers barriers to entry and enables even non-traditional firms to offer in-house financing competitive financial products. As a result, the financial services industry has seen a surge in competition, which fosters greater innovation and diversification of services offered to consumers.

Investing in this burgeoning sector presents a lucrative venture for several reasons. First, the ongoing integration of new technologies—such as artificial intelligence, blockchain, and big data analytics—continues to enhance the efficiency and appeal of FinTech services, drawing more consumers away from traditional banking methods. Moreover, the FinTech sector’s ability to adapt rapidly to changing consumer behaviors and preferences stands out as a significant advantage, especially in an era where consumers increasingly demand convenience, speed, and customization. Lastly, the financial returns and growth potential in this dynamic sector make it an attractive opportunity for investors looking to capitalize on the latest trends in financial services.

In this comprehensive guide, we delve into the essential components necessary for starting a successful lending company. From selecting the appropriate lending business model to securing the funding needed for your new venture, this article outlines the key steps and considerations that will put you on the path to establishing a thriving financial enterprise. Whether you’re exploring traditional lending practices or innovative financial technologies, following this guide will equip you with the knowledge and strategies needed to navigate the complexities of the financial sector and build a prosperous lending business.

When starting a lending company, choosing the right lending business model is crucial as it defines how you will operate, interact with borrowers, manage risks, and achieve profitability. Here are some of the prominent lending models you can consider, each catering to different business goals and resources:

Characteristics:

- Structure: Connects individual borrowers and lenders directly via an online platform, bypassing traditional financial institutions

- Regulation: Less regulated than traditional banking, but still subject to financial service regulations.

- Clientele: Attracts tech-savvy individuals and small businesses seeking alternatives to conventional banks.

Best for Startups and tech companies that aim to leverage technology for financial services and are interested in a faster, more flexible lending process.

Characteristics:

- Structure: microfinance lenders provide small loans to underserved populations, typically in developing regions, to promote entrepreneurship.

- Regulation: Varies significantly but generally lighter than that for traditional banks.

- Clientele: Individuals or small groups lacking access to traditional banking services.

Best for NGOs, social enterprises, and businesses looking to make a social impact alongside financial returns, especially in emerging markets.

Characteristics:

- Structure: A merchant cash advances lender provides funds to businesses in exchange for a percentage of daily credit card sales plus a fee.

- Regulation: Generally viewed as commercial transactions rather than loans, hence less regulated.

- Clientele: Small to medium-sized businesses needing quick access to capital with consistent credit card sales.

Best for Lenders looking for high returns on short-term investments and businesses with high credit card sales volume but perhaps less-than-perfect credit.

Characteristics:

- Structure: payday loan lenders offer short-term, high-cost loans that are typically due by the next payday.

- Regulation: Heavily regulated due to concerns over high-interest rates and predatory practices.

- Clientele: Individuals with poor credit scores needing immediate cash flow

Best for Lenders in markets with high demand for short-term financing options and a robust regulatory framework to manage the associated risks.

Characteristics:

- Asset-based Lending: Hard money loans are typically secured by real estate property. The loan amount is based primarily on the value of the property used as collateral, not on the borrower’s creditworthiness.

- Short-term Nature: These loans are usually offered for short durations, ranging from a few months to a few years, making them suitable for borrowers looking for quick, temporary financing.

- Higher Interest Rates: Due to the higher risk associated with less emphasis on the borrower’s credit score, hard money loans command higher interest rates compared to traditional bank loans.

- Speed of Funding: Hard money lenders can often provide quick approvals and funding, which is critical for borrowers involved in time-sensitive real estate transactions, such as auctions or foreclosure purchases.

- Less Stringent Requirements: The approval process for hard money loans is generally less stringent than that for traditional loans. Lenders focus more on the collateral and the project’s potential than on the borrower’s financial history.

Best for Lenders that specialize in the real estate market.

When creating a business lending blueprint, it is important to consider factors such as the lending model you will use.

- Market Needs: What does your target market lack in terms of current lending options?

- Regulatory Environment: How complex are the regulations in your region, and what can you realistically comply with?

- Risk Tolerance: How much risk are you willing to take on, especially concerning defaults and market volatility?

- Resource Availability: Do you have the technology, capital, and expertise to manage the chosen lending model effectively?

Each model has its distinct setup and operational requirements, so align your choice with your strategic business goals and operational capabilities.

In the preliminary stage of product development, it is critical to concentrate on establishing a well-defined value proposition. It is paramount to define this proposition and test it with the intended audience before tackling any other tasks. The primary goal is to create a lending product that addresses a specific pain point for the desired market.

Product-market fit in the lending industry can be broken down into three critical components:

- The Client (Target Audience): Who are your potential customers? What are their characteristics, financial behaviors, and needs?

- The Problem (Client Need): What specific financial gaps or issues are your potential customers facing that current market offerings are not addressing effectively?

- The Solution (Your Product): How does your product address these needs uniquely or more effectively than the competition?

It is imperative to identify the target audience who requires the product, address a specific issue, and present a solution they are willing to pay for.

For instance, In the context of microfinance, the target clients are typically low-income individuals or small business owners in developing regions who lack access to traditional banking services. These clients often face significant barriers to economic growth, such as the absence of collateral and low credit scores, which prevent them from securing conventional loans. The problem these clients encounter is multifaceted: not only do they need small-scale financing to grow their businesses or meet personal needs, but they also require flexible repayment terms that align with their irregular income patterns.

A microfinance lending product should address these issues by providing small, unsecured loans with minimal eligibility requirements. The solution needs to be designed as straightforward and accessible, offering loans based on the borrower’s character and business potential rather than on formal credit histories.

Interest rates are generally higher than those of traditional banks but are made affordable to accommodate the clients’ financial constraints. Additionally, the microfinance model often includes training and support for borrowers, helping them develop financial literacy and business skills that are crucial for long-term success.

To be successful in building fit-to-market products, continuously improve your product, pricing, and processes, tailoring your product features to meet specific client needs, and differentiate your offerings from traditional financial products to capture and retain your target market.

Starting a lending business involves investment, but it’s important to recognize that customer acquisition often accounts for a larger share of expenses. Personal loan lending is notably competitive, with numerous firms competing for the same customer base. This competition drives up the cost of marketing and customer acquisition as business lending companies, particularly those offering private lending services, invest significantly in marketing initiatives to stand out in online lending businesses. Establishing a sound strategy for acquiring customers and controlling costs by targeting specific prospects most effectively and economically is crucial.

Many businesses make the mistake of prioritizing customer base growth over profitable unit economics. They operate under growth-driven models that prioritize the rapid expansion of their user base to quickly achieve economies of scale, even if it means offering a product with unfavorable unit economics.

This approach can result in aggressive spending on customer acquisition to capture large market shares before competitors.

A critical component of success in the lending industry is cultivating repeat business, which hinges on delivering reliable customer service and leveraging an advanced technology platform to enhance the customer experience. For instance, if you are planning to start a payday loan business, there exists a robust and consistent demand for emergency funds, especially pronounced among Millennials and Generation Z. These demographics are adept at digital solutions and share the service expectations of younger generations. By adopting sophisticated payday loan software, lenders can tap into and effectively serve this burgeoning market segment.

Consistently meeting and exceeding customer expectations with prompt, attentive service fosters loyalty and trust, which are essential for securing repeat patronage.

Let‘s explore effective marketing practices for acquiring a solid customer base in the financial services sector.

The growth of a financial services business often relies on direct marketing strategies. These can encompass various channels such as direct mail campaigns, digital marketing (including platforms like Facebook and Google), television commercials, and outdoor advertising like billboards and subway ads. The key to a successful direct marketing campaign lies in its distinctiveness and difficulty to replicate. Rather than relying solely on broad tactics like purchasing AdWords for loan-related searches—which face stiff competition from banks and established financial players—a more strategic approach is to either focus on a niche demographic with specific lending needs or to develop an innovative marketing channel.

A niche marketing tactic in direct marketing for a lending business could involve creating customized financial solutions for a specific profession or industry. For example, offering specialized loan products to healthcare professionals, such as doctors and nurses, who might need quick access to funds due to irregular payment cycles or high upfront costs for equipment or continued education. This strategy could be executed through partnerships with medical associations or by attending medical conferences to engage with this demographic directly.

Another approach could be to target entrepreneurs and small business owners by offering expedited loan origination processes and entrepreneurial support services. This niche group often requires quick loans to capitalize on immediate business opportunities or to manage cash flow during slow seasons. Tailored marketing campaigns could be run on professional networking sites like LinkedIn or through direct partnerships with business incubators and local chambers of commerce, where these entrepreneurs are likely to seek advice and resources.

By focusing on such distinct segments and understanding their unique financial needs, a lending business can design direct marketing initiatives that speak directly to these customers’ pain points, fostering a connection that general marketing tactics may not achieve.

Another effective method for acquiring borrowers is through strategic partnerships with companies. For instance, Greensky successfully partnered with Home Depot to offer the Greensky credit card directly at Home Depot’s points of sale. Similarly, Affirm has partnered with online merchants to facilitate financing options right at the online checkout. This B2B2C (Business-to-Business-to-Consumer) or B2B2B (Business-to-Business-to-Business) strategy, though challenging due to long enterprise sales cycles, can significantly enhance borrower acquisition. Once a partnership is established, it can provide a continuous flow of borrowers at a relatively low customer acquisition cost (CAC).

Furthermore, targeting underserved customer segments, such as the unbanked or small and medium enterprises (SMEs) with tailored products or services can also be highly effective. Globally, approximately 1.7 billion adults are without access to traditional banking services. Fintech companies that cater to these segments by offering innovative products, such as online lending in emerging markets, have not only filled a critical gap but have also proven that serving the unbanked can be both profitable and operationally efficient. By adopting such approaches, lending businesses can tap into new markets and drive growth through unique, hard-to-replicate acquisition channels.

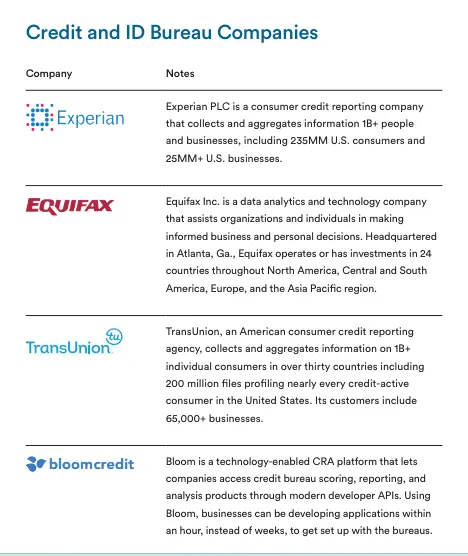

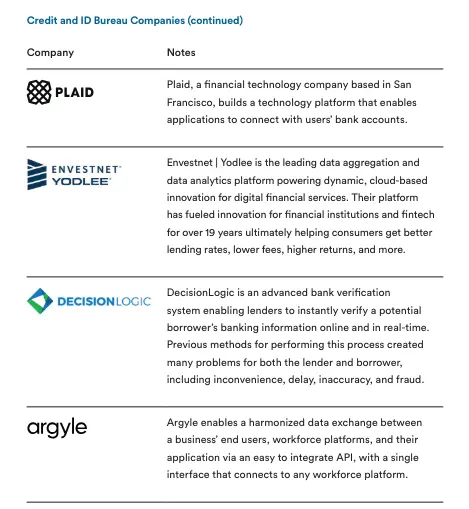

After developing strategies to market to and acquire borrowers, companies must focus on identifying and leveraging diverse data sources to power their underwriting and credit decision processes. Traditionally, Credit Bureaus have been the primary data providers, but the landscape has evolved with the entry of numerous alternative data providers.

image 1. Credit and ID Bureau Companies

Many companies have started to harness internal data effectively for credit decisioning. For example:

In Southeast Asia, Telecom data is being used to underwrite consumers with limited credit history (Lenddo).

In the U.S., payment data is utilized to assess creditworthiness for small and micro businesses (Square), while cash flow data aids in underwriting small business loans (Kabbage).

Supply chain data is employed for underwriting factoring services (Amazon).

Trade school performance data is used by Climb Credit to make lending decisions.

Moreover, as a significant number of potential borrowers, particularly those who are underbanked or residing outside the traditional credit markets of the U.S., Canada, and the European Union, do not possess FICO scores, there is a pressing need for alternative, reliable data sources that can accurately predict risk. By exploring and integrating these unconventional data sources, companies can extend their services to these underserved populations, opening up new markets.

Lending is a unique business where you loan money to customers and hope they pay it back. The key is to make a profit from those who repay their loans and minimize losses from those who don’t. It’s important for lenders to figure out the right balance between making money from reliable customers and losing money from those who default. This helps in deciding who to lend to while avoiding two types of mistakes: one where you miss out on lending to good customers (leaving money on the table), and another where you mistakenly lend to those who end up not paying back.

Companies in this start-up phase should focus on experimental design and data collection strategies. Investing time and resources in gathering comprehensive data will enable them to develop more accurate and efficient risk models and underwriting strategies as the business matures. Additionally, effective back-end risk management allows companies to broaden their acquisition strategies confidently.

To maintain a healthy loan portfolio and minimize defaults, it is imperative to employ robust risk assessment models, effective collection strategies, and fraud detection measures.

Analyzing vast amounts of data with cutting-edge AI technology can reveal patterns that enhance the speed and precision of credit decision-making, further improving reliability. The latest trends in risk management to utilizing AI and ML tools enable financial institutions to refine customer segmentation. These tools can identify specific variables that may not be evident to human analysts, allowing for the creation of more accurate segmentation rules. The capability to identify specific variables helps in tailoring products and services to fit the unique needs of different customer segments, especially providing better access to credit for underserved borrowers. enhancing customer satisfaction and loyalty.

Once you have the data and model ready, you can proceed to develop a loan software stack that facilitates loan application decision-making. While you have the option to build this component using in-house development teams, outsourcing it to a specialized software company may be a more cost-effective and quicker alternative.

When choosing commercial lending software for your business, it can be challenging to determine the best loan management option. A loan origination system’s primary purpose is to support you in achieving strategic objectives. Before selecting a loan management software solution, consider what your organization values most and what you hope to accomplish with the software. Cost, features, and customer service are all factors to consider during the process of automated loan origination software selection. A free trial business lending software allows users to test the product, understand its functionalities, and assess if it delivers the correct value before purchasing. CompassWay offers a 14-day free trial period for end-to-end lending software to help you get familiar with the commercial lending software solution.

Starting a private lending company requires careful financial planning and a robust understanding of the capital needed to sustain operations and facilitate growth. Initially, determining the right product-market fit and having a clear grasp of the metrics outlined in your business plan is crucial. These foundational elements not only guide your business strategy but also shape how potential investors view your venture

Funding for an online lending business often begins with equity, typically from the founders or early investors. However, as the business scales, this approach alone becomes unsustainable. The nature of lending necessitates a reliable flow of capital to fund loans, necessitating a shift towards raising debt. Interestingly, there’s a noticeable pattern in debt financing: smaller, short-term loans are often easier to secure and manage because they carry less risk and allow for quicker returns on investment, making them more attractive to lenders.

As the company grows and demonstrates potential for high returns, particularly in underserved or booming markets, it may attract the attention of venture capitalists. These investors might offer capital in exchange for equity in the company, providing a significant boost but also diluting ownership. It’s important to note that raising debt is a gradual process. Securing your first line of credit is typically the most challenging hurdle, as it requires convincing lenders of your company’s viability and potential for profit.

In essence, the amount of money needed to start a private lending company can vary widely depending on several factors, including the scale of operations, targeted loan sizes, and the regulatory environment. Entrepreneurs must be prepared for significant initial capital outlay to cover operational costs and the first round of loans, with ongoing funding strategies to support scalability and stability.

As we conclude our exploration of starting a private lending company, it’s important to recognize the sector as an emerging investment opportunity that is just beginning to attract the attention of both institutional and individual investors. Despite its complexities and challenges, the private lending industry presents a fertile ground for innovation and profitability, drawing in those who are keen to leverage new financial technologies and methodologies. This nascent interest is driven by the high potential for returns and the increasing demand for alternative financing solutions that are not adequately served by traditional financial institutions.

The growing traction in the private lending space underscores a shift in investment strategies, where more investors are looking beyond conventional markets in search of higher yields and diversification. As the industry continues to evolve and mature, it offers a promising frontier for those willing to navigate its unique risks and opportunities. Therefore, entering the private lending market now could position early adopters at a strategic advantage, allowing them to shape the future of this dynamic sector and potentially reap significant benefits as the market expands.

Navigation: